Make VAT easier with Fiduly

Sign-up for 30 days free trial, no credit card needed.

Sign-up for 30 days free trial, no credit card needed.

This guide explains how to configure and manage VAT in Fiduly. You will find the steps to generate a VAT statement, configure VAT rates, enter your VAT number, manage registration during the financial year and understand the differences between the effective method and the net tax rate method.

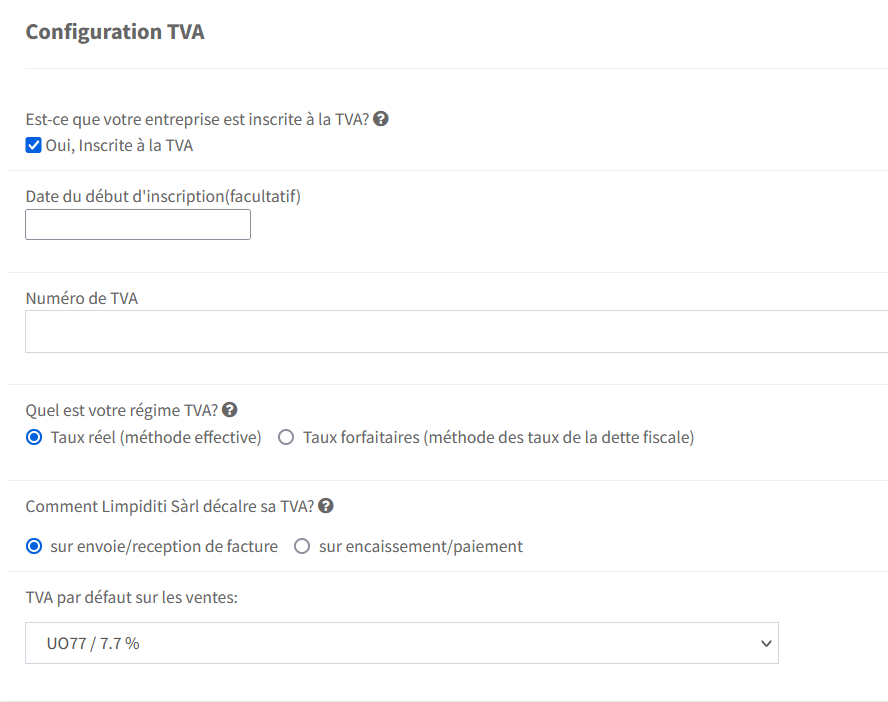

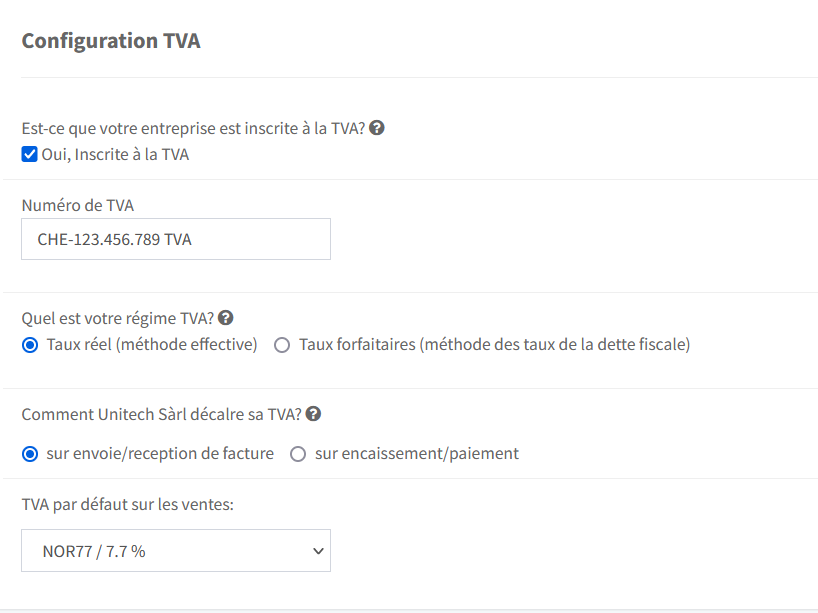

In the navigation menu, go to “Settings”, then “Settings” and choose “VAT”.

In the navigation menu, go to “Settings”, then “Settings” and choose “VAT”.

VAT settings also affect the creation of your invoices. For invoicing, see our page Swiss invoicing software with VAT and QR-bill.

VAT has an impact on your accounting procedures. There are two ways to report it:

Effective method (reporting the turnover generated and the input tax incurred): you must submit a VAT statement every quarter.

Reporting using flat tax rates: you must report your turnover, including the VAT charged to your customers, every six months and multiply it by the net tax rate approved by the Federal Tax Administration (FTA). In this way, input tax is deducted at a flat rate and does not need to be calculated separately.

You must submit the VAT statement without being prompted within 60 days after the end of the reporting period and pay the tax due at the same time. If the FTA owes you a tax credit for a reporting period, the amount will be refunded within 60 days after receipt of the VAT statement.

The question of when, meaning in which reporting period, you must declare the tax and deduct input tax depends on the reporting method you choose. Normally, the date on which the invoice is sent or received is decisive. However, you can request authorization to declare the tax and input tax in the reporting period in which the invoice is paid. You must follow the chosen reporting procedure for at least one tax period, meaning one calendar year.

All companies that are required to pay value added tax must report their VAT. However, they must also choose the method they will use: the effective method or reporting based on flat tax rates, also known as the net tax rate method. The accounting requirements vary depending on the method chosen.

What are the differences?

Net tax rate method (flat rate)

Many small businesses choose this method for their VAT statements because it reduces administrative complexity. On the one hand, they only have to submit VAT statements every six months instead of every quarter. On the other hand, using the flat tax rate also makes it unnecessary to calculate input tax separately.

The effective method

The effective VAT reporting method requires companies to report the income generated as well as the accumulated input tax. Companies that choose the effective reporting method must submit their VAT statements to the Federal Tax Administration (FTA) on a quarterly basis, within 60 days after the end of each quarter. The same deadline applies to payment due dates.

How is VAT calculated with the net tax rate method?

For companies submitting their VAT statements based on flat tax rates, the tax due is calculated as follows: total sales, including the VAT charged to customers, are multiplied by the flat tax rate. This reduced VAT rate must be approved by the Federal Tax Administration (FTA) and depends on the company’s business sector. The advantage of this VAT reporting method is clear: input tax is included as a flat-rate amount and does not need to be reported separately.

The Federal Tax Administration offers this simplified VAT statement method for companies with turnover below CHF 5.005 million, including VAT, and a tax liability of no more than CHF 103,000 per year. These companies can choose to submit VAT based on the flat tax rate, which is lower than the standard rate of 8.1%, provided they waive the standard input tax deduction procedure, which would otherwise be deducted from the VAT collected on turnover. This simplified taxation method must be maintained for at least one year, and VAT statements only need to be submitted twice a year, unlike the usual quarterly reporting.

Before generating a VAT statement, make sure that your invoices, expenses, payments and accounting entries are complete and correctly recorded. Accounting errors can affect the amount of VAT to be declared.

To check entries and account statements, see our guide managing accounting in Fiduly.

Find answers to the most frequently asked questions about managing VAT with Fiduly.

Yes. If your company is subject to VAT, Fiduly allows you to generate a VAT statement based on the invoices, expenses and accounting entries recorded.

VAT rates are configured from the settings menu, in the VAT rate settings tab.

Yes. You can configure your VAT number in your company’s VAT settings.

Yes. You can enter the VAT registration date when the company becomes subject to VAT during the financial year.

With the effective method, the company declares VAT on turnover and deducts input tax. With the net tax rate method, reporting is simplified and depends on an approved rate based on the business activity.

It is recommended to check that invoices, expenses, payments and accounting entries are complete and correctly recorded before generating the VAT statement.